The market moved. Then it corrected.

Demand for autonomous revenue agents is enormous — and the failure mode is consistent. What survives a security review, proves ROI, and earns buyer trust is governed autonomy: agents execute, humans approve.Here's what the data says, seat by seat, for the six roles on a typical revenue committee.

Key takeaways

- →The macro opportunity is real: McKinsey estimates generative AI could add $2.6–$4.4T annually, with marketing and sales among the largest concentrations of value.

- →Then the reckoning: analysts now describe governance — not capability — as the bottleneck, and expect 40%+ of agentic AI projects to be cancelled by end of 2027.

- →The prescription isn't more autonomy — it's governed identities, least privilege, audit trails, and staged autonomy behind approval gates.

- →That is a specification for how to deploy agents, and it's the architecture the Revenue Accelerator was built on before it became consensus.

Two years of hype, one clear correction

The macro opportunity is real and large. McKinsey estimates generative AI could add the equivalent of $2.6–$4.4 trillion annually, with roughly three-quarters of the value concentrated in four areas — one of which is marketing and sales. Gartner projects that by 2028, 90% of B2B buying will be intermediated by AI agents, pushing more than $15 trillion of B2B spend through agent-to-agent exchanges.

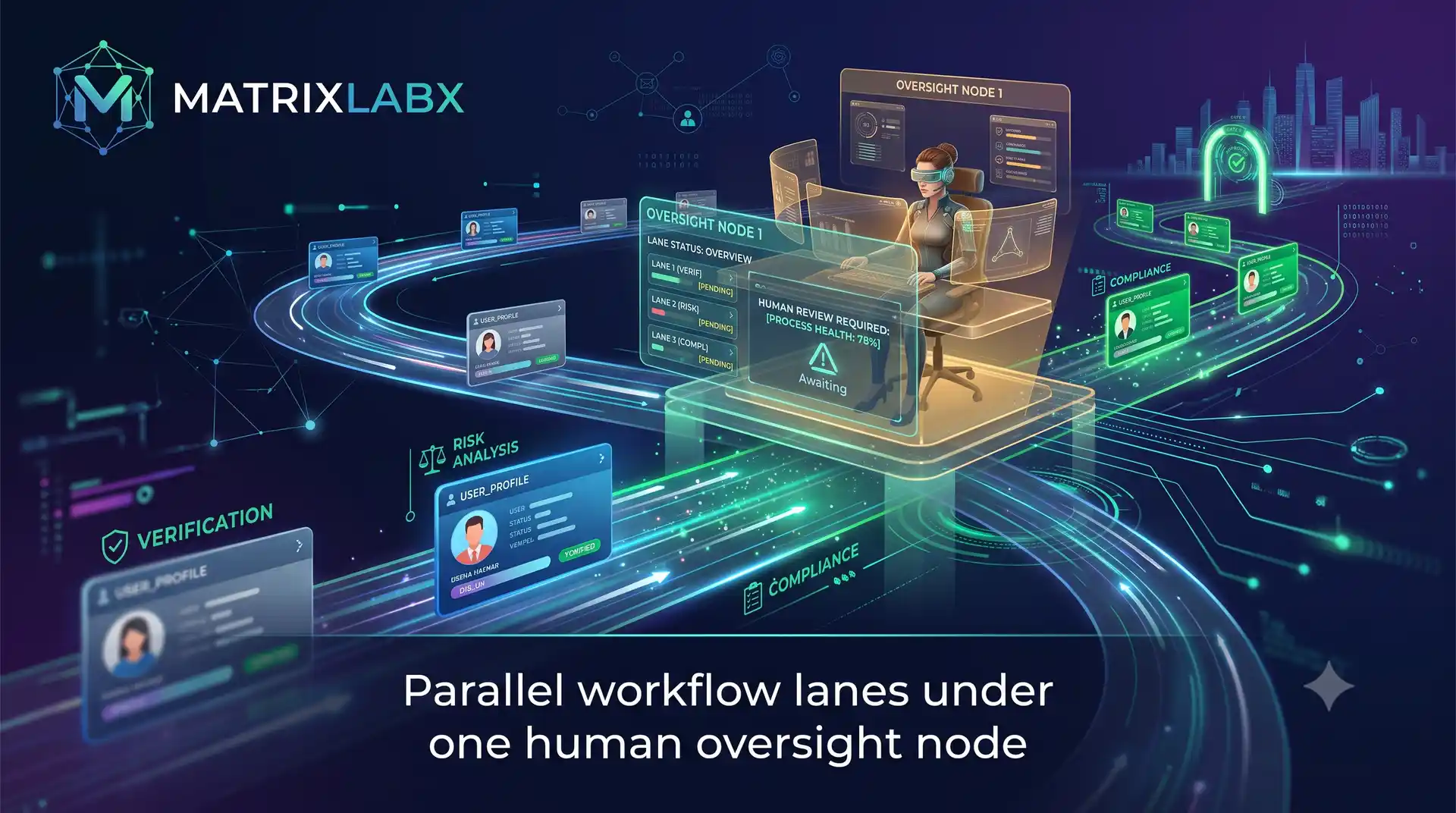

Then the reckoning. The same analysts now describe governance — not capability — as the bottleneck. The prescription they write is not more autonomy. It is governed identities, least privilege, audit trails, and staged autonomy behind approval gates. That is a specification for how to deploy agents — and it's the architecture the Revenue Accelerator was built on before it became consensus.

How to read the figures. Industry statistics are third-party benchmarks, attributed to their named source, included for market context. MatrixLabX outcome figures are labeled by measurement status — Measured (live today), Target (modeled vs. a human/copilot baseline; validated per client via the free AAR), Case (a single named account), or Inherited (a Google Cloud platform capability). Nothing here is a guaranteed result; every Target is validated on your own data before any commitment.

The revenue committee · six seats

CRO / VP Revenue

Metric owned · pipeline velocity

What the data says

Activity is up and yield is down. Reps now spend only about 40% of their week actually selling (Salesforce, State of Sales 2026), and the average rep burns nearly two full days a week on admin (Forrester activity research). Roughly 78% of sellers missed quota in 2025, up from ~69% the year before. The teams closing the gap pair reps with AI: Gartner finds sellers who partner effectively with AI are 3.7× more likely to hit quota, and Bain attributes ~30% productivity gains to AI-assisted selling.

The fit

The CRO's ceiling isn't effort — signals now fire faster than a human team can act, and adding reps means linear cost and a multi-month ramp. The Prospecting and Outbound agents run the full loop continuously and a human approves every consequential send — lifting the ceiling without inheriting the ungoverned-bot failure mode.

Read the CRO's guide to autonomous pipeline generation →Modeled vs. human/copilot baseline. Validated per client via the free AAR.

Modeled vs. manual touch volume per rep.

Instrumented live today.

CFO

Metric owned · CAC / cost per pipeline dollar

What the data says

Acquisition cost is structurally fixed — seats, retainers, headcount — paid whether or not output lands. And the CFO now sits inside the AI budget conversation precisely because value has been hard to prove: Forrester found only ~15% of AI decision-makers saw an EBITDA lift, and fewer than one in three can connect AI spend to P&L. The buying pattern is shifting from flat per-seat licenses toward consumption and outcome-linked models.

The fit

Labor-as-a-Service: you pay for executed workflows and delivered outcomes, not seats sitting at partial utilization. Fixed cost becomes variable and results-linked. The entry point is diligence beforespend — the free AAR models a client-specific P&L on your own data before any commitment.

Read the CFO's guide to autonomous digital workforce economics →Modeled; validated per client via the free AAR.

Spend tracks executed workflows, metered per action — not a percentage claim.

COO

Metric owned · output per headcount

What the data says

In the old model, output is coupled to payroll — more volume means more people doing manual middleware: routing, reconciliation, follow-up. Bain estimates AI could roughly double the share of time sellers spend actually selling (~25%→50%). The upside is real when the plumbing is right: Salesforce reported that in-house, agents worked 130,000 previously untouched leads and generated 3,200 opportunities in four months.

The fit

Digital labor decouples output from the payroll line. Agents execute end-to-end, humans stay on approval, so volume scales without the headcount line scaling with it — more durable than RPA (breaks on process change) or offshore BPO (trades rate for latency and QC).

Read how autonomous agents replace headcount in mid-market ops →Modeled vs. manual touch volume per rep.

Instrumented in the live demo.

VP Growth / PLG Owner

Metric owned · trial-to-paid conversion

What the data says

In product-led motions, conversion is decided early and most trials die quietly before the value event, with no one watching in real time. Speed of response is the lever — Salesforce's 2026 research shows sellers expect agents to cut research time ~34% and drafting time ~36%, freeing exactly the reaction speed a stalling trial needs. Across the market, AI-using teams reported 83% revenue growth last year versus 66% for teams without AI.

The fit

Analytics surface a stall after the fact; lifecycle email is pre-scheduled and blind to the moment. The Trial Conversion agent monitors in-product behavior in real time and drafts a personalized activation sequence at the stall moment, for a human to approve and fire. It acts — it doesn't just render an insight.

Read why PLG funnels leak 40% of signups before activation →Modeled. Requires trial-telemetry instrumentation across a cohort.

RevOps Champion

Metric owned · CRM accuracy / time-to-value

What the data says

CRM data rots continuously — decay outpaces quarterly cleanups. ZoomInfo data indicates reps lose ~27% of their time to inaccurate data; Validity found 37% of CRM users report lost revenue tied directly to poor data quality; yet Forrester found only ~29% of revenue teams run a formal data-quality process, and Gartner pegs the average annual cost of poor data quality at $12.9M per organization. In the agent era, data quality is now cited as a top blocker to putting agents into production.

The fit

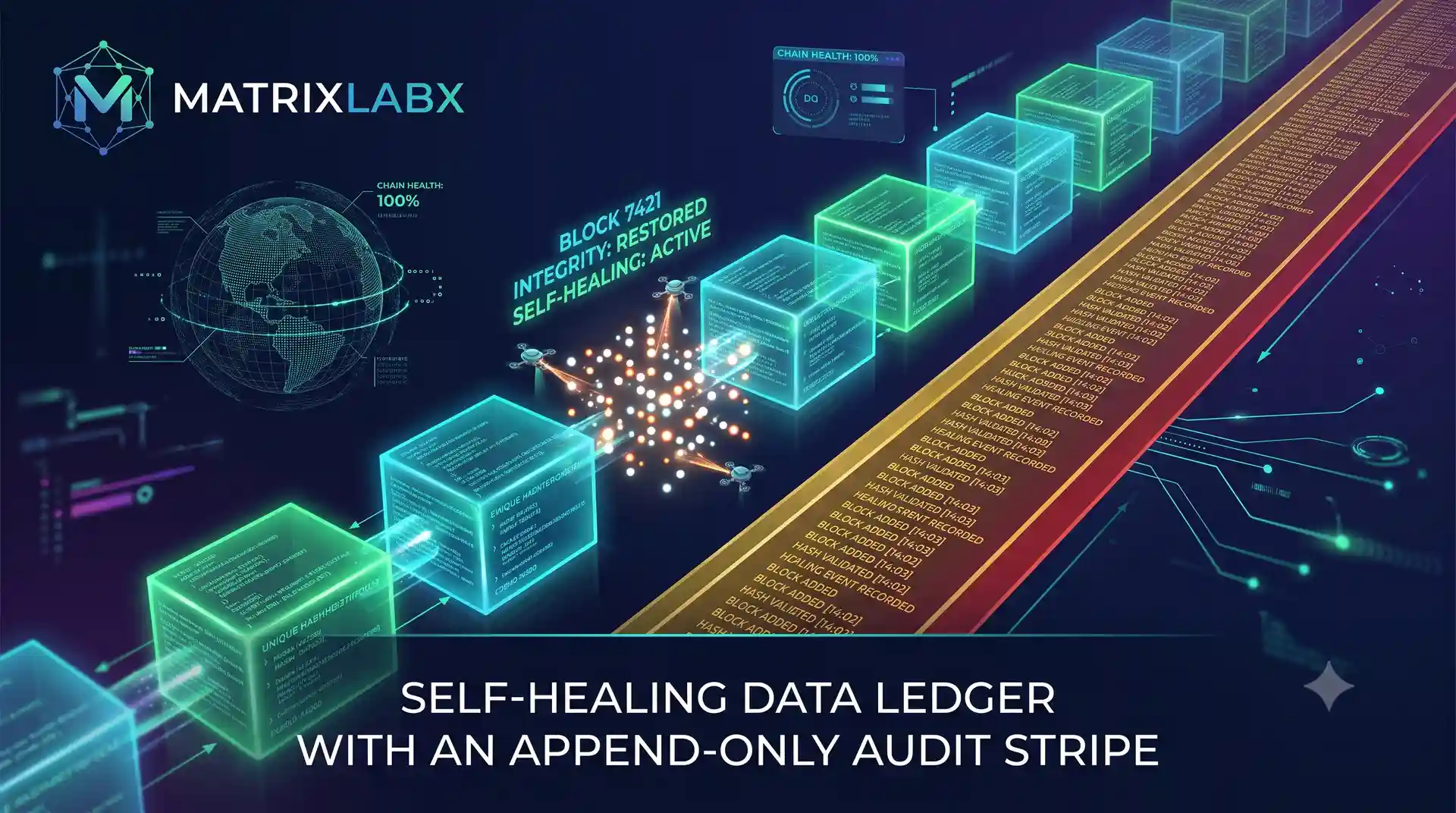

The Revenue Accelerator is designed to execute around imperfect data out of the box, and every change it makes is logged immutably — governance and hygiene in one motion rather than a separate cleanup project.

Read how CRM debt costs manufacturing tech companies their best buyer signals →Delivery commitment; validated per client.

Measured post-deploy.

Delivered by a separate Data Health product — not one of the four Revenue Accelerator agents. Distinction kept explicit.

CIO / Security

Metric owned · data perimeter / governance

What the data says

This is where the correction bites hardest — and where PrescientIQ™ has its strongest claim. Forrester's 2026 outlook warns an autonomous-agent deployment is likely to cause a major enterprise breach this year: a majority of organizations still lack AI governance policies, most security teams have already observed risky agent behavior, and a plurality of security pros now rank agentic AI a top emerging attack vector. Crucially, Forrester notes human-in-the-loop is useful but insufficient on its own — at scale you also need enforceable policy, least-privilege identity, and audit trails.

The fit

That is the exact specification the Revenue Accelerator was built to. Agents run inside your own Google Cloud tenant under VPC Service Controls — data never leaves your perimeter. Each agent carries a least-privilege identity, Model Armor provides runtime protection, and every action lands in an immutable, glass-box audit trail. The approval gate is one control among several, not the only one.

Read how regulated FinServ companies cut CAC without losing the audit trail →Google Cloud platform capability — defensible today, attributable to the platform, not our application layer.

Inherited platform attributes — not MatrixLabX-held certifications. App-layer SOC 2 in progress.

Every target above is validated on your data first

The free Autonomous Audit Report maps these targets to your own environment — your pipeline, your CAC, your trial cohort, your data — and produces a client-specific P&L projection before you commit a dollar. Diligence first. Then decide.

Request your free AAR →Source index · third-party benchmarks

| Figure | Source |

|---|---|

| Gen AI value $2.6–$4.4T annually; ~75% in four areas incl. marketing & sales | McKinsey (2023–25) |

| 90% of B2B buying agent-intermediated by 2028; >$15T through agent exchanges; agents outnumber sellers ~10:1 | Gartner (2025) |

| 40%+ of agentic AI projects cancelled by end 2027; ~130 “real” agentic vendors | Gartner (2025) |

| 75% of B2B buyers prefer human-led experiences by 2030 | Gartner (2025) |

| Reps partnering with AI 3.7× more likely to hit quota; 72% overwhelmed by tools | Gartner (2024–25) |

| ~40% of week selling; 87% use AI; 54% used agents; ~34%/36% research/drafting cut; 83% vs 66% revenue growth; 130k leads → 3.2k opps | Salesforce, State of Sales (2026) |

| ~78% of sellers missed quota in 2025; ~2 days/week on admin | Salesforce / Forrester (2025–26) |

| ~30% productivity gain from AI-assisted selling; selling time could ~double | Bain (2025) |

| ~15% EBITDA lift reported; <⅓ tie AI to P&L; ~25% of AI spend deferred to 2027 | Forrester, Predictions 2026 |

| Agentic breach likely 2026; majority lack AI governance; most security teams saw risky agent behavior | Forrester 2026 security outlook |

| Rep time lost to bad data ~27%; 37% report lost revenue; 29% run formal data-quality process; poor data quality ~$12.9M/yr | ZoomInfo · Validity · Forrester · Gartner |

| Google Cloud attestations (SOC 2 / ISO 27001 / PCI DSS; HIPAA via BAA) | Google Cloud / Gemini Enterprise Agent Platform docs |

Benchmarks are third-party industry figures included for context. MatrixLabX outcome figures remain Measured / Target / Case / Inherited as labeled above.

See the governance architecture built for this correction

Book a 30-minute discovery call. We'll walk through the governed-autonomy loop and audit ledger with your revenue and security teams together.

Book a Discovery Call →George Schildge

Founder & Chief AI Officer, MatrixLabX

George Schildge founded MatrixLabX to resolve the tension revenue leaders face between the pressure to deploy autonomous agents and the governance bar security and compliance teams now require — building the approval gate and audit ledger into the agent architecture itself, rather than treating it as an afterthought.

Go deeper: the cluster articles

CRO / VP Revenue

Read the CRO's guide to autonomous pipeline generation

CFO

Read the CFO's guide to autonomous digital workforce economics

COO

Read how autonomous agents replace headcount in mid-market ops

VP Growth / PLG Owner

Read why PLG funnels leak 40% of signups before activation

RevOps Champion

Read how CRM debt costs manufacturing tech companies their best buyer signals

CIO / Security

Read how regulated FinServ companies cut CAC without losing the audit trail